Categories

08 Jul, 2026

Savvy Tips

Your credit score directly determines the interest rate your credit card charges, and the difference between an excellent and a poor score can be 10 to 15 percentage points of APR on the same card product. On a $5,000 balance, that spread translates to $500 to $750 in additional annual interest. Understanding this connection, and knowing what actually moves your score in the short and medium term, is one of the highest-return activities in personal finance.

10-15%

APR difference between excellent and poor credit

30%

of FICO score determined by credit utilization

76%

of cardholders who get a rate cut just by asking

6 pts

average APR reduction when cardholders call and ask

How credit card APRs are set

Credit card APRs in the US are not fixed. They are set as the prime rate plus a spread called the margin, which the issuer determines based on the applicant's credit profile at the time of approval. When the Federal Reserve adjusts the federal funds rate, the prime rate moves accordingly, and variable APRs on most credit cards adjust automatically, typically within one billing cycle. This is why the average credit card APR rose from around 16% in early 2022 to above 24% by late 2023 as the Fed raised rates 11 times.

Within this framework, individual cardholders receive APRs that vary from the issuer's lowest advertised rate, reserved for applicants with the highest credit profiles, to the highest rate in their disclosed range, for applicants who just barely qualify. The gap between these rates is typically 10 to 14 percentage points, and your credit score is the primary variable determining where in that range you land.

What the score ranges mean for actual APRs

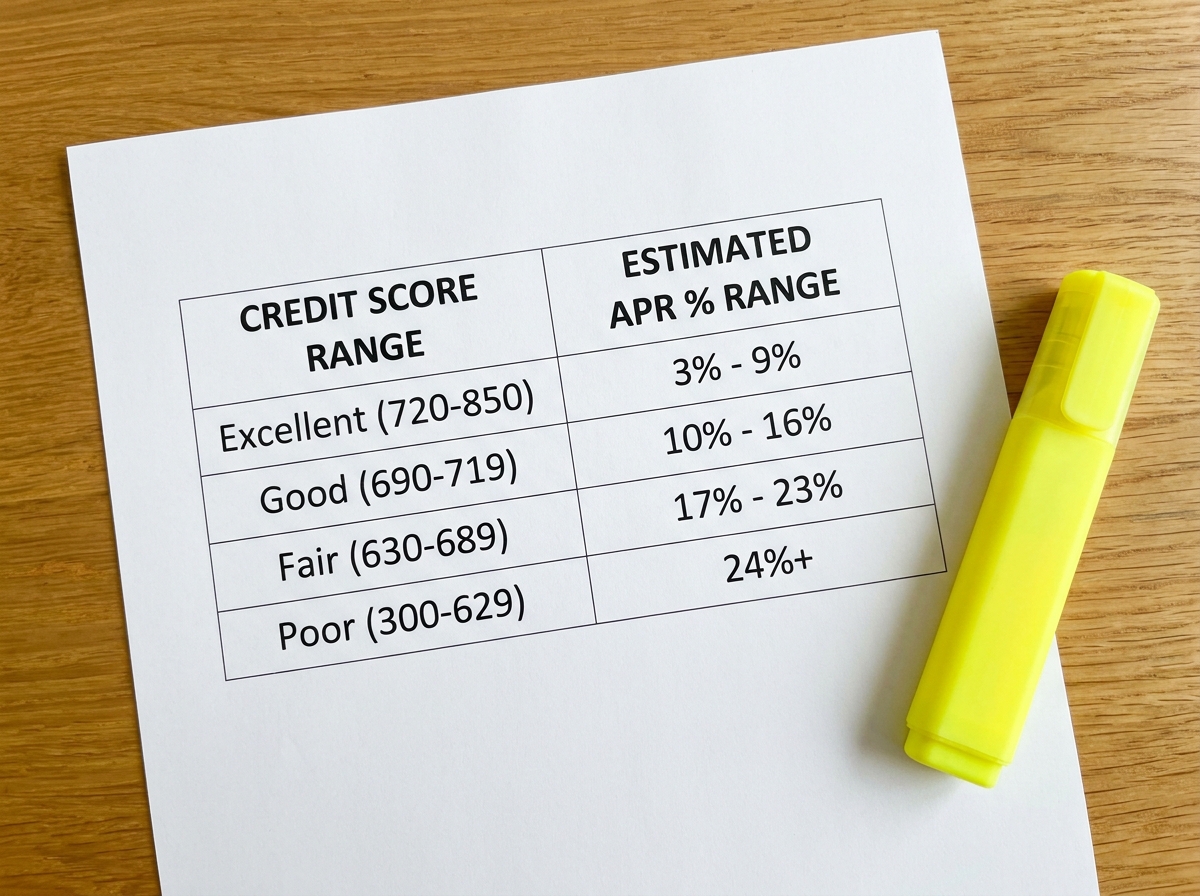

Using current market rates as of early 2026, a cardholder with a FICO score of 800 or above typically receives the lowest APR tier a given issuer offers, currently around 19 to 21% for most issuers. A score of 740 to 799 receives the middle tier at approximately 22 to 25%. A score of 670 to 739 lands in the upper tier at 25 to 28%. Below 670, issuers that offer credit at all typically price it at 28 to 30%, and subprime products or secured cards run at 29.99% or above.

These differences compound quickly. On a $10,000 balance making minimum payments only, a cardholder at 20% APR pays approximately $8,200 in interest over the life of the debt. The same cardholder at 29% APR pays approximately $18,000 in interest. Credit score management is, in this context, a direct financial instrument with measurable dollar outcomes.

The five factors and which ones you can move quickly

FICO scores are calculated from five weighted factors: payment history at 35%, credit utilization at 30%, length of credit history at 15%, credit mix at 10%, and new credit inquiries at 10%. Two of these, payment history and utilization, account for 65% of your score and are the ones you can most directly influence in the short term.

Utilization, the ratio of your current balance to your total credit limit across all revolving accounts, is the fastest-moving factor in FICO calculations. It is recalculated each time a new statement balance is reported, typically monthly. Paying down a balance from 40% utilization to 10% can produce a score increase of 20 to 50 points within one to two billing cycles. This is the only lever in personal credit management that works within weeks rather than months or years.

Payment history changes more slowly but has the highest long-term impact. Seven years of on-time payments builds a track record that keeps your score in the top tiers regardless of other factors. A single missed 30-day payment can drop your score by 50 to 110 points and takes about two years of clean history to fully recover from.

Credit Score APR Savings Calculator

See how much you would save annually in interest if you improved your credit score.

Requesting a lower APR from your current issuer

Most cardholders with improving credit profiles do not realize they can request a lower APR without applying for a new card. A 2023 LendingTree survey found that 76% of cardholders who called and specifically requested a rate reduction received one, with an average reduction of 6 percentage points. The issuer runs a soft inquiry, confirms your current creditworthiness, and adjusts the rate if your profile has improved since the account was opened. The call takes five minutes and the only downside is that they say no.

This is particularly effective if your score has improved by 50 or more points since you opened the account, if you have been a customer for more than two years, and if you have no missed payments on the account. Call the number on the back of your card, state that you would like to request an APR review based on your improved credit profile, and have your score handy to reference if asked.

The utilization and limit increase strategy

The most common score optimization strategy for people carrying high balances is to request a credit limit increase on existing cards, which reduces utilization without changing behavior. If you have $8,000 in balances across cards with a combined $15,000 in limits, your utilization is 53%, which is damaging to your score. If those same limits increase to $25,000 with the same balances, utilization drops to 32%, which improves your score by 20 to 40 points. Limit increase requests are typically approved via soft inquiry for cardholders with strong payment histories.

Frequently asked questions

How much can I lower my credit card APR by improving my score?

Moving from a score of 680 to 760 or above typically repositions you from the high-rate tier to the low-rate tier within the same issuer, a difference of 5 to 10 percentage points depending on the card. The practical path is to pay down balances to reduce utilization, maintain on-time payments, and then call the issuer to request a rate review once your score has improved. The issuer can adjust your rate on an existing account without requiring a new application.

Does applying for a new credit card affect my APR on existing cards?

Not directly. Hard inquiries from new card applications temporarily lower your score by 5 to 10 points, and a lower score could theoretically affect your standing with existing issuers if they perform a periodic account review. In practice, most existing card APRs are set at account opening and only change if you specifically request a review or if the issuer adjusts rates in response to Federal Reserve rate changes, which applies to all cardholders equally.

Should I close high-APR cards once I pay them off?

Generally no. Closing a card reduces your total available credit, which increases your overall utilization ratio and can hurt your score. If the card has no annual fee, keeping it open with no balance and an occasional small purchase preserves the credit limit and account age benefits. The exception is a card with a high annual fee that you are not recouping in value. In that case, first try requesting a product change to a no-fee version before closing the account outright.