Categories

03 Jun, 2026

Savvy Tips

Approximately 45 million Americans have no usable credit score, and tens of millions more are stuck below 620 with limited access to competitive financial products. The problem is structural: most lenders want to see credit history before extending credit, but you need a lender to extend credit before you can build history. The way out of this loop is a specific sequence of steps, not a single product or shortcut.

45M

Americans with no usable credit score

6 mo

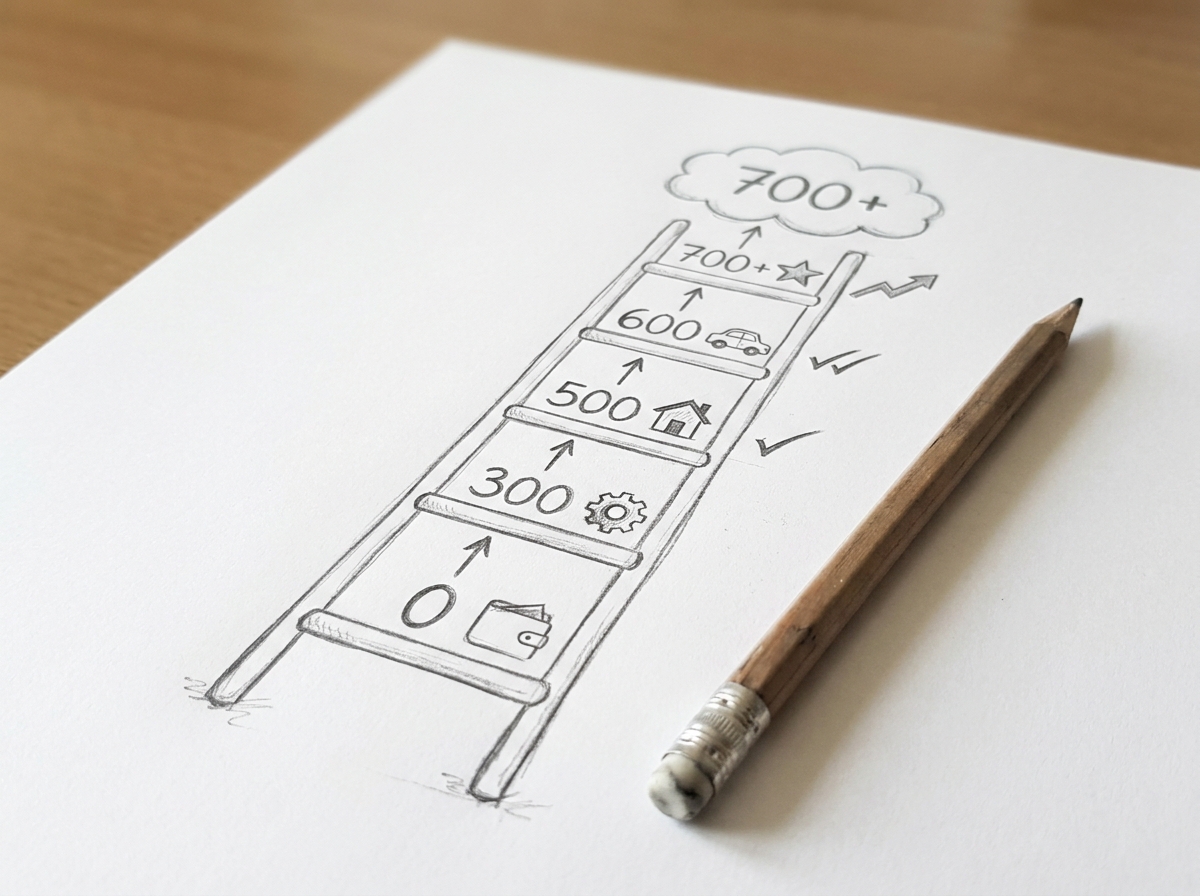

to generate your first FICO score

12-18 mo

typical timeline to reach a 700+ score

$0

annual fee on the best secured cards

Why credit building is harder in 2026

The rate environment of 2022 to 2025 made issuers more conservative with thin-file applicants. Credit limits on secured cards are lower than they were three years ago, approval standards have tightened, and several issuers have reduced their secured card offerings or added fees. None of this makes credit building impossible. It makes the starting sequence more important than it has been in years.

The fastest path: become an authorized user

If you have a family member or close friend with a long credit history, clean payment record, and low credit utilization, being added as an authorized user on their account is the fastest credit-building move available. You do not need to use the card or even have it in your possession. Within 30 to 60 days, the account's history appears on your credit report, often generating your first FICO score immediately if you had none.

This only works when the primary account is in good standing. A high-utilization or delinquent account transfers those negatives to your file as well. Verify with the primary cardholder that their issuer reports authorized users to all three bureaus, which most major issuers do. If no such person is available, move to the next step.

Open a no-fee secured credit card

A secured card requires a cash deposit that becomes your credit limit. From the credit bureau's perspective, a secured card is reported identically to any other revolving credit account: payment history, utilization, and account age all factor into your score. Put one or two small recurring charges on the card each month, pay the full balance before the due date, and let the account age.

The best secured cards in 2026 charge no annual fee. Discover it Secured and Capital One Platinum Secured are the most commonly recommended, both because they charge no annual fee and because they offer a clear path to an unsecured upgrade after 12 to 18 months of on-time payments. Avoid any secured card charging more than $35 per year in fees. That cost does not accelerate credit building and reduces the net value of the product significantly.

Keep your balance below 10% of your credit limit at statement close to maximize the score benefit. A $500 secured card where you charge $50 per month and pay it off builds your score faster than one where you charge $400 and carry a balance.

Add a credit builder loan

Credit builder loans are offered by credit unions, community banks, and online lenders including Self and Credit Strong. Unlike traditional loans, you do not receive the money upfront. The lender places the loan amount in a savings account, you make monthly installment payments, and each on-time payment is reported to the bureaus. At the end of the term, you receive the principal you paid in.

The credit benefit comes from adding an installment account alongside your revolving credit card. FICO models favor having both account types, a factor called credit mix that accounts for around 10% of your score. For someone starting from zero, combining a secured card and a credit builder loan builds a more complete credit profile faster than either product alone. Typical loan amounts are $500 to $1,500 over 12 to 24 months at fees of $15 to $25 per month depending on the lender.

Credit Builder Timeline Calculator

Estimate how long it takes to reach a target credit score based on your starting point and products.

What the timeline actually looks like

FICO generates your first scoreable profile after six months of account history. Most people following this sequence, one secured card and one credit builder loan with consistent on-time payments and low utilization, see their first score in the 630 to 680 range at month six. By month 12, consistent behavior typically pushes the score to 670 to 720. By month 18 to 24, the range for most people in this situation is 720 to 750, which unlocks competitive rates on unsecured cards, personal loans, and auto financing.

The most common disruption to this timeline is a missed payment. Even one 30-day late mark stays on your credit report for seven years and causes a score drop of 50 to 110 points depending on your current score level. If cash flow is tight, call the issuer before the payment becomes 30 days late. Most issuers will defer a payment or waive a late fee for a first-time caller with an otherwise clean record.

Mistakes that slow the process

Applying for multiple credit products in a short period is the most common mistake. Each application generates a hard inquiry that temporarily lowers your score by 5 to 10 points and remains on your report for two years. Multiple inquiries in a 60-day window signal financial stress to lenders. Open one product, give it six months to establish history, then consider adding a second if needed.

Closing your first secured card when you upgrade to an unsecured product is another frequent error. The account age and payment history on your original card continue benefiting your score as long as the account remains open. If the issuer returns your deposit and upgrades the product, you get both outcomes with no action required. If you must close it, do so only after you have other accounts with several years of age.

Frequently asked questions

How long does it take to go from no credit to a 700 score?

With a secured card, a credit builder loan, and on-time payments, most people reach 700 within 12 to 18 months. The timeline depends on whether you can also become an authorized user, which accelerates the first score generation significantly. Someone added to a five-year-old account with good history may score above 700 within their first year. Someone starting from nothing with only a secured card typically hits 700 between months 14 and 20.

Does checking my own credit score hurt it?

No. Checking your own score is a soft inquiry, which has no effect on your score. Hard inquiries, which occur when you apply for new credit, are the ones that create a temporary score reduction. You can check your own score as often as you want without any credit impact. Most banks and card issuers now offer free credit score monitoring as a cardholder benefit, including Capital One, Discover, and many credit unions.

Can I build credit without anyone's help?

Yes. The secured card and credit builder loan combination works without an authorized user account. It takes a few months longer to generate your first score, but the outcome is the same. Some rent reporting services, including Experian RentBureau and Rental Kharma, also add rental payment history to your credit file for a monthly fee, which can accelerate score generation if you have a strong rental payment track record.