Categories

26 Apr, 2026

Savvy Tips

The average American household carrying credit card debt owes $6,501. That number has climbed steadily since 2021, and at the standard 24.37% APR that most Americans now pay, it doubles in under four years if you only pay the minimum. Getting out is not complicated. It requires a plan and the discipline to stick with it for six to eighteen months.

$6,501

average US credit card debt per household

24.37%

average US credit card APR (2025)

30+ yrs

payoff time at minimum payments

76%

of cardholders who got a rate cut just by asking

$6,501

average US credit card debt per household

24.37%

average US credit card APR (2025)

30+ yrs

payoff time at minimum payments

76%

of cardholders who got a rate cut just by asking

Why minimum payments are a debt trap

Credit card companies are required by law to show the minimum payment impact on your statement. Most people glance at it and keep scrolling. On a $6,500 balance at 24.37% APR, paying only the minimum (roughly 2% of the balance, around $130) takes over 30 years to clear and costs more than $14,000 in interest alone. The card issuer makes more money from your debt than from the purchase itself.

Every dollar you pay above the minimum directly reduces the principal, which reduces future interest charges. A $200 payment instead of $130 on that same balance cuts payoff time from 30 years to under 5. That is the entire mechanism of debt freedom: consistently paying more than the minimum.

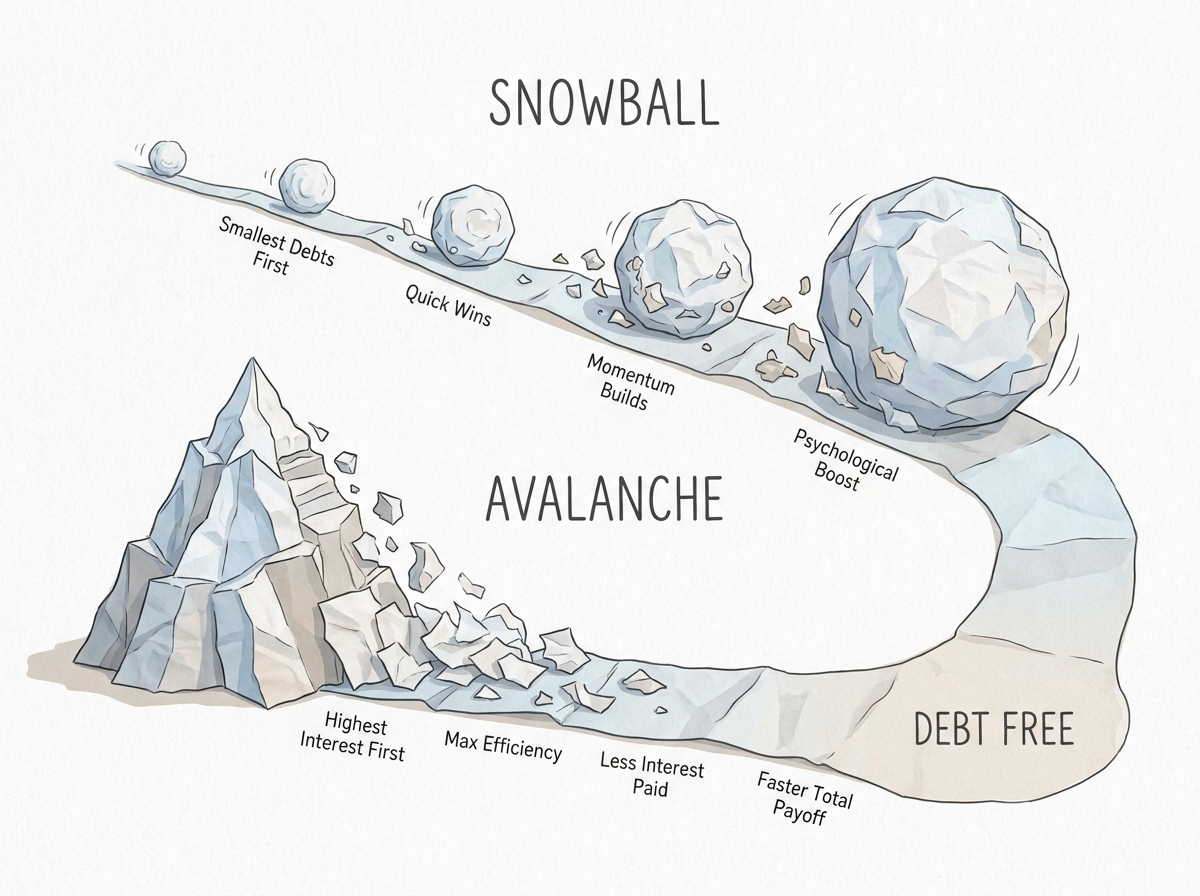

The two proven payoff strategies

Two methods dominate personal finance advice and both work. The right one depends on your psychology, not the math.

The avalanche method pays the card with the highest interest rate first while making minimums on all others. Mathematically optimal. You pay less interest overall and get out of debt faster on paper. The downside is that it can feel slow if your highest-rate card also has the largest balance. Progress is invisible for months.

The snowball method pays the card with the smallest balance first, regardless of rate. You get wins faster. Research from the Harvard Business Review confirms that the psychological momentum from clearing accounts accelerates total repayment in real-world settings, even though the math on paper is slightly less efficient. For most people, motivation matters more than optimization.

Choose one and automate it. Set up automatic payments for minimums on all cards, then direct every additional dollar to your target card manually each payday.

Finding extra money without a side hustle

You do not need a second job to accelerate debt payoff. You need to redirect money that is already leaving your account each month.

- Subscription audit: The average American pays for 4.5 streaming and digital subscriptions they rarely use. A 20-minute audit typically frees $40 to $80 per month.

- Balance transfer card: If your credit score is above 670, a 0% APR balance transfer offer (typically 12 to 21 months) can eliminate interest entirely during the payoff period. Watch the 3 to 5% transfer fee and do the math before applying.

- Negotiate your rate: A 2023 LendingTree survey found that 76% of cardholders who called and asked for a lower APR received one. The average reduction was 6 percentage points. One phone call, no cost.

- Tax refund deployment: The average federal refund runs around $3,100. Directing it straight to your highest-rate card can cut payoff time by 12 to 18 months.

Credit Card Debt Payoff Calculator

Enter your balance, APR, and monthly payment to see your payoff timeline and total interest cost.

Credit Card Debt Payoff Calculator

Enter your balance, APR, and monthly payment to see your payoff timeline and total interest cost.

The balance transfer strategy explained

A balance transfer moves your existing debt to a new card offering 0% interest for a promotional period. This is the most powerful tool available to people with good credit and a concrete payoff plan. Without a plan, it simply delays the problem and adds another card to manage.

The math: moving $6,500 to a card with a 3% transfer fee and 18-month 0% APR costs $195 upfront. At 24.37%, you would have paid over $1,400 in interest over those same 18 months. Net savings of more than $1,200, assuming you pay it off before the promo period ends. If you do not, the remaining balance reverts to the regular APR, often 27 to 29%, which compounds fast.

Best balance transfer cards in 2026 offer 15 to 21 months at 0%, with a one-time fee of 3 to 5%. Compare the fee against projected interest savings before applying.

What not to do

Two mistakes consistently extend payoff timelines. The first is using credit cards for new purchases while paying down debt. Every new charge erodes progress and creates a psychological anchor that makes the debt feel permanent. Remove the cards from your wallet during the payoff period. The accounts stay open and your credit score stays intact.

The second mistake is using home equity loans or lines of credit to pay off card debt. Swapping unsecured debt for debt secured by your home is a risk transfer that most financial counselors advise against unless the alternative is bankruptcy.

Building the habit that keeps you out

Debt payoff is a one-time project. The habit that prevents you from returning is simpler: never carry a balance you cannot pay off in full within two billing cycles. That single rule, applied consistently, turns credit cards into a cashback and rewards tool rather than a financing mechanism.

Frequently asked questions

Will paying off credit card debt hurt my credit score?

No, it will help it. Credit utilization, which is the ratio of your balance to your credit limit, accounts for about 30% of your FICO score. Paying down balances reduces utilization and raises your score. Do not close the cards after paying them off, because closing accounts reduces your available credit and can temporarily lower your score.

How long does it actually take to pay off credit card debt?

At the average US balance of $6,500 and an APR of 24.37%, a $300 monthly payment clears the debt in about 28 months. A $500 monthly payment cuts it to under 16 months. The variable is how much extra you can direct to the card each month beyond the minimum.

Is debt consolidation a good idea?

A personal loan consolidating multiple high-rate cards into one fixed payment at a lower rate can simplify repayment and reduce total interest. It works best when the loan rate is significantly lower than your average card rate and you stop using the cards after transferring the balance. Without that discipline, consolidation often leads to a second round of card debt on top of the loan.